Choosing the right credit card in India 2026 feels more like solving a puzzle than making a financial choice. With hundreds of options—ranging from UPI-linked RuPay cards to premium travel rewards—most people end up with a card that costs them more in fees than it gives back in benefits. At Equitylogy, we believe a credit card should be a tool for wealth, not a trap for debt. Whether you’re looking to build your CIBIL score from scratch, save on your monthly grocery bills, or get free lounge access at the airport, this guide breaks down the hidden terms banks don’t tell you and helps you find the perfect plastic for your pocket.

What Is a Credit Card? – Meaning, & Types

Credit Card: A credit card is a financial tool issued by banks or financial institutions that allows you to borrow funds up to a pre-approved limit to make purchases or withdraw cash. Unlike a debit card, which pulls money directly from your bank account, a credit card is essentially a short-term loan.

Different Types of Credit Cards in India

Not all cards are created equal. Depending on your lifestyle, you should choose a card that rewards your specific spending habits:

- Shopping & Cashback Cards: Best for those who shop frequently on Amazon, Flipkart, or Myntra. You get direct cashback or heavy reward points.

- Travel Credit Cards: Perfect for frequent flyers. These offer free airport lounge access, air miles, and travel insurance.

- Fuel Credit Cards: Designed to save money on petrol and diesel through “fuel surcharge waivers” and extra reward points at gas stations.

- Rewards Credit Cards: Versatile cards that give you points for every rupee spent, which can later be redeemed for vouchers or products.

- Secured Credit Cards: These are issued against a Fixed Deposit (FD). These are excellent for beginners or those trying to repair a bad CIBIL score.

- UPI-Linked RuPay Cards: The newest trend in India! These allow you to link your credit card to UPI apps like GPay or PhonePe to scan and pay at local shops.

Compare Best Credit Cards & Top 10 credit card in India

| Card Name | Best For | Annual Fee | Key Highlight |

|---|---|---|---|

| HDFC Regalia Gold | Premium Lifestyle | ₹2,500 | Complimentary Club Marriott & Lounge Access |

| SBI Cashfllck | Online Shopping | ₹999 | 5% Cashback on almost all online spends |

| ICICI Amazon Pay | Amazon Lovers | Lifetime Free | Unlimited 5% cashback for Prime members |

| Axis Flipkart | Flipkart & Myntra | ₹500 | 5% Unlimited cashback on Flipkart |

| HDFC Tata Neu Infinity | UPI & Tata Brands | ₹1,499 | 5% NeuCoins on UPI (via Tata Neu App) |

| SBI BPCL Octane | Fuel Savings | ₹1,499 | 7.25% Value back on Fuel (BPCL) |

| Amex Platinum Travel | Milestone Rewards | ₹5,000 | ₹40,000+ worth of vouchers on reaching milestones |

| IDFC First Wealth | Low Interest/Lounge | Lifetime Free | Low APR & 2 Complimentary Airport Lounges/month |

| Airtel Axis Bank | Utility Bills | ₹500 | 25% Cashback on Airtel Bills & Utilities |

| HDFC Millennia | Beginners/Gen Z | ₹1,000 | 5% Cashback on top brands like Swiggy & Zomato |

How to Choose the Best Credit Card: The Quick Decision Guide

Finding the right card doesn’t have to be complicated. Instead of looking at what the bank offers, look at how you spend. Use this table to match your lifestyle with the perfect card category.

Step 1: Match Your Spending Category

| If Your Main Expense Is… | You Should Look For… | Why? |

|---|---|---|

| Online Shopping | Cashback Cards | Direct 5% savings on sites like Amazon & Flipkart. |

| Grocery & Utilities | Reward/Points Cards | High reward multipliers on daily household essentials. |

| Daily Local Commute | Fuel Cards | To get fuel surcharge waivers and cashback at petrol pumps. |

| Travel & Vacations | Travel/Miles Cards | For free airport lounge access and airline vouchers. |

| Small Local Purchases | RuPay Credit Cards | To link with UPI (GPay/PhonePe) for “Scan & Pay.” |

Step 2: Evaluate the True Cost

Before applying, compare these three critical factors to ensure the card is actually free for you.

| Factor | What to Check | Expert Pro-Tip |

|---|---|---|

| Annual Fee | Is it ₹0 (Lifetime Free) or ₹500 – ₹5000? | Only pay a fee if the rewards exceed the cost. |

| Spend Waiver | Can the fee be waived? | Most cards waive the fee if you spend ₹1-2 Lakh a year. |

| Interest Rate | What is the monthly APR? | Always pay in full to keep interest at 0%. |

Step 3: The Final Eligibility Checklist

Use this checklist to avoid a CIBIL score drop from rejected applications:

- Age: Must be between 21 & 60 years.

- Employment: Salaried / Self-Employed with a steady income.

- CIBIL Score: A score of 750+ guarantees the best cards and limits.

- Documentation: PAN Card, Aadhaar, and last 3 months salary slips/ITR.

Best Cashback Credit Cards in India (2026 Comparison)

Cashback cards are the most popular choice in India because they offer real value that you can see directly in your monthly statement. Instead of complicated points, you get “Real Money” back.

Here is a short, human-curated comparison of the top cashback credit cards for 2026.

| Card Name | Best For | Cashback Rate | Annual Fee |

|---|---|---|---|

| SBI Cashback Card | All-Rounder | 5% on all online spends | ₹999 |

| ICICI Amazon Pay | Amazon Shopping | 5% for Prime Members | Lifetime Free |

| Axis Flipkart | Flipkart & Myntra | 5% Unlimited Cashback | ₹500 |

| Airtel Axis Bank | Utility Bills | 25% on Airtel/Utilities | ₹500 |

| HDFC Millennia | Gen-Z / Dining | 5% on Swiggy, Zomato, etc. | ₹1,000 |

| HSBC Live+ | Groceries/Dining | 10% on Dining/Groceries | ₹999 |

Tip: Kabhi bhi credit card se ATM se cash na nikalein, ispar 3-4% monthly interest lagta hai.”

Top 10 Best Rewards & Lifestyle Credit Cards (2026)

This section highlights the most rewarding lifestyle cards currently available in India. These cards are specifically designed for those who want their daily spending to pay for their next luxury experience or domestic getaway.

| Card Name | Best For… | Annual Fee | Standout Lifestyle Perk |

|---|---|---|---|

| HDFC Regalia Gold | Luxury Travel | ₹2,500 | Free Club Marriott & M&S/Reliance vouchers. |

| Amex Platinum Travel | Milestone Rewards | ₹5,000 | ₹40k+ value in Taj/IndiGo vouchers on ₹4L spend. |

| SBI Elite | Movie Buffs | ₹4,999 | Free Movie Tickets (worth ₹6,000/year) + Lounge. |

| Axis Select | Dining & Golf | ₹3,000 | BOGO on BookMyShow & Priority Pass membership. |

| IDFC First Wealth | Low APR & Perks | Lifetime Free | 2 Free Movie Tickets & 2 Spa visits per month. |

| SBI Prime | All-rounder | ₹2,999 | 20 Points per ₹100 on Birthdays + Utility rewards. |

| Standard Chartered Ultimate | Direct Rewards | ₹5,000 | Flat 3.33% Reward Rate (highest in its class). |

| HDFC Diners Club Black | High Spenders | ₹10,000 | Unlimited Global Lounge & 2x Rewards on Weekend dining. |

| Axis Magnus | HNI Lifestyle | ₹12,500 | Concierge services & luxury brand vouchers. |

| AU Zenith | Tier-2 City Luxury | ₹7,999 | Dedicated Personal Concierge & 10k Welcome Points. |

Top Travel Credit Cards in India (2026 Comparison)

Traveling in 2026 is all about smart lounge access and zero forex markups. Here are the top picks to help you travel like a VIP without the heavy price tag.

| Card Name | Best For | Annual Fee | Key Travel Benefit |

|---|---|---|---|

| Axis Atlas | Milestone Rewards | ₹5,000 | Direct “Edge Miles” for flights & hotels. |

| Amex Platinum Travel | Free Vacations | ₹5,000 | Up to ₹40,000 worth of Taj & Indigo vouchers. |

| HDFC Regalia Gold | All-Rounder | ₹2,500 | Priority Pass & Club Marriott membership. |

| SBI ELITE | Luxury Perks | ₹4,999 | Free Movie Tickets & International Lounges. |

| IDFC First Wealth | Low Cost Travel | Lifetime Free | Zero Forex Markup on international spends. |

| AU IXIGO Card | Train & Flight | ₹999 | Zero payment gateway fees on Ixigo app. |

| Scapia Federal | Digital Nomads | Lifetime Free | Unlimited domestic lounge access (on spend). |

3 Things to Check Before Picking a Travel Card

- Forex Markup: If you travel abroad, look for cards with 0% to 1% markup. Standard cards charge 3.5%, which is very expensive.

- Lounge Access Type: Some cards only offer Domestic lounge access. If you travel outside India, ensure the card offers International Lounge via Priority Pass or Dreamfolks.

- Point Devaluation: Check if the reward points can be converted to your favorite airline (like Air India, Vistara, or Singapore Airlines) at a good ratio.

Best Fuel & Utility Credit Cards: 2026 Comparison

Fuel and utility bills are recurring expenses that everyone has to deal with. Choosing a card specifically for these can save you thousands of rupees annually through surcharge waivers and accelerated reward points.

| Card Name | Best For | Top Benefit | Fuel Surcharge Waiver |

|---|---|---|---|

| SBI BPCL Octane | High Fuel Spends | 7.25% Value back at BPCL pumps | 1% (Up to ₹100/month) |

| Airtel Axis Bank | Utility & Phone Bills | 25% Cashback on Airtel bills & 10% on Utilities | 1% (Up to ₹500/month) |

| ICICI HPCL Super Saver | HPCL Fuel & Daily Needs | 5% Reward points on fuel & departmental stores | 1% (At all HPCL outlets) |

| Axis Indian Oil | Budget Fuel Users | 4% Value back at IOCL outlets | 1% (At all IOCL outlets) |

| HDFC Tata Neu Infinity | UPI & Utility Spends | 5% NeuCoins on Utility via Tata Neu App | 1% (On min. ₹400 spend) |

| Standard Chartered Super Value Dash | All-Round Utilities | 5% Cashback on Fuel, Phone, and Electricity | 1% (Up to ₹200/month) |

Quick Tips for Maximizing Value

- Stick to the Network: If you have an Indian Oil card, you will only get maximum benefits at Indian Oil pumps. Using it at BPCL will give you standard rewards.

- Watch the Caps: Most cashback on utility bills (like electricity or water) is capped per month (e.g., ₹250 or ₹300).

- The Surcharge Rule: To get the 1% surcharge waiver, your fuel transaction usually needs to be between ₹400 and ₹4,000.

- Utility via UPI: If you use a RuPay variant like the Tata Neu Infinity, you can earn rewards even when paying local utility bills via UPI apps.

Best Premium & Super-Premium Credit Cards in India (2026)

When you move into the super-premium segment, you aren’t just looking for cashback; you are looking for exclusive experiences. These cards offer the highest reward-to-spend ratios and luxury lifestyle benefits.

| Card Name | Best For | Annual Fee | Luxury Highlight |

|---|---|---|---|

| HDFC Infinia (Metal) | The Ultimate All-rounder | ₹12,500 + GST | 1:1 Reward ratio for travel & unlimited lounge |

| Axis Bank MAGNUS | Lifestyle & Rewards | ₹12,500 + GST | Buy One Get One on movies & premium concierge |

| SBI Aurum | Invite-Only Luxury | ₹9,999 + GST | Dedicated 24×7 butler service & golf perks |

| Amex Platinum Card | Global Travel & Status | ₹60,000 + GST | Access to Centurion Lounges & Doheny lifestyle |

| ICICI Emeralde Private | Low Interest & Travel | ₹12,499 + GST | No cancellation charges on travel & low APR |

Why Choose a Super-Premium Card?

- Global Lounge Access: Most of these cards offer an unlimited Priority Pass for both the primary holder and guests.

- Concierge Service: A personal assistant to book your flights, fine-dining tables, or event tickets.

- High Reward Redemption: While basic cards offer 0.25p per point, these cards often offer ₹1 per point or air mile.

- Golf Privileges: Complimentary access to premium golf courses across India and the world.

Eligibility for Super-Premium Cards

Since these are high-end products, the banks have strict criteria:

- Income: Usually requires a monthly salary of ₹2 Lakh – ₹3 Lakh+ or an ITR of ₹30 Lakh+.

- Credit Score: A pristine CIBIL score of 780 or above.

- Existing Relationship: Many of these (like Infinia or Aurum) are often offered on an invite-only basis to existing high-value customers.

How to Use Credit Cards for UPI Payments: A 2026 Guide

Gone are the days when you had to carry a physical wallet or worry about a low bank balance for small daily purchases. In 2026, linking your RuPay Credit Card to apps like PhonePe, Google Pay, or BHIM has changed the game.

Why should you link your Credit Card to UPI?

- Earn Rewards on Small Spends: Earn points even on your daily tea or grocery runs where you previously used bank transfers.

- Interest-Free Period: Use the bank’s money for 45–50 days while keeping your savings account balance intact to earn interest.

- Improved CIBIL Score: Regular, small UPI transactions via credit card and timely bill payments can help boost your credit history faster.

The Hidden Rules You Must Know:

- RuPay Only: Currently, only RuPay variant credit cards can be linked to UPI. Visa and Mastercard variants are generally not supported for Scan & Pay at local merchants.

- Merchant Category Matters: You can pay any merchant (shopkeeper) with a QR code, but you cannot send money to a friend’s personal bank account using a credit card via UPI.

- No Extra Charges (Up to ₹2000): Most small merchant transactions are free for the user, but some high-value transactions might have specific merchant restrictions.

Step-by-Step: How to Link Your Card

- Open your preferred UPI App (PhonePe, GPay, or Paytm).

- Go to your Profile and select Add Credit Card/Link Credit Card.

- Choose your Bank (Make sure your mobile number is the same).

- The app will fetch your RuPay card details.

- Set your UPI PIN using your card’s expiry date and CVV.

- Start Scanning! Simply scan any merchant QR and select your credit card as the payment source.

The Ultimate Checklist for First-Time Credit Card Users

Getting your first credit card is like getting the keys to a powerful car—it can take you places, but only if you know how to drive it safely. Before you swipe for the first time, make sure you tick these boxes:

1. The Before You Apply Stage

- Check Your CIBIL Score: Even for a basic card, a score of 750+ is ideal. If you have no score, look for “FD-based” credit cards.

- Verify Income Documents: Keep your last 3 months’ salary slips or ITR (Income Tax Return) ready.

- Identify Your Spending Habit: Do you spend more on groceries (Cashback cards), travel (Lounge/Miles cards), or online shopping (Rewards cards)?

2. The Once the Card Arrives Stage

- Check the Welcome Kit: Ensure the credit limit mentioned is what you were promised.

- Enable/Disable Online Transactions: Use the bank’s app to set limits on ‘International’ and ‘Contactless’ (Tap and Pay) transactions to prevent fraud.

- Link to UPI (If RuPay): Follow our guide above to link it to GPay or PhonePe for easy daily use.

3. The Financial Discipline Rules (Golden Rules)

- The 30% Rule: Try not to use more than 30% of your total credit limit. Using ₹30,000 out of a ₹1,00,000 limit keeps your CIBIL score healthy.

- Total Amount Due > Minimum Amount Due: Never pay just the “Minimum Amount.” Banks charge 40%–50% annual interest on the remaining balance.

- No Cash Withdrawals: Never use your credit card at an ATM. The interest starts the very second the cash comes out.

4. The Safety First Habits

- Set a Billing Reminder: Set an alarm for 3 days before the due date. Late payment fees are heavy and hurt your credit history.

- Review Monthly Statements: Spend 5 minutes every month checking for “hidden” insurance or subscription charges you didn’t authorize.

Credit Card Settlement vs. Closed: Which is Better for CIBIL?

If you have struggled with debt, you might face a choice: Settlement or Closing. To find the best credit card in India later, you must protect your score now.

- Closed: This means you paid every single paisa back (Principal + Interest). It shows as “Closed” on your CIBIL report, which is excellent for your future loan eligibility.

- Settled: This means the bank agreed to accept a lower amount than what you owed. While the debt is gone, your CIBIL report will show Settled. This is a red flag for lenders and can stop you from getting a top 10 credit card in India for years.

- The Verdict: Always aim to Close your account. If you have already settled, try to pay the remaining “haircut” amount later to convert the status to Closed.

Rejection Reasons for Salaried Employees (Even with a 750 Score)

It is frustrating to have a good score and still get rejected for a premium credit card in India. Common reasons include:

- Recent Inquiries: If you applied for 3-4 cards in the last month, you look credit hungry.

- Negative Area/Office Pin Code: Some banks blacklist specific locations due to past fraud data.

- Low Debt-to-Income Ratio: If 50% of your salary already goes to EMIs, banks won’t give you another card.

- Missing Fixed Line/Verification: Some top 10 premium credit cards in India still require a physical office landline or a successful home visit.

Best Credit Card for UPI Payments (Salary Under ₹20,000)

If your salary is under ₹20,000, you don’t need a heavy metal card. You need a most powerful credit card in India for daily utility—the RuPay variant.

- Top Pick: HDFC Tata Neu Plus or Axis Indian Oil RuPay.

- Why: These cards link directly to GPay/PhonePe. Even on a smaller salary, you can earn 1-2% back on every local tea stall or grocery scan, which was impossible with Visa/Mastercard.

How to Remove Late Payment Marks from a Credit Report

A single late payment can stop you from getting the top 10 lifetime free credit card in India.

- Goodwill Letter: If it was a one-time mistake, write a Goodwill Letter to the bank manager requesting a waiver.

- Dispute via CIBIL: If the mark is an error, raise a dispute on the official CIBIL portal with proof of payment.

- Pay the Dues: The mark stays for 7 years, but its impact reduces as the entry gets older.

Credit Card Lounge Access List India (2026 Update)

Lounge access rules have changed significantly this month. Most top 10 credit cards in India now require a “Spend-Based” criteria.

- The Rule: You usually need to spend ₹35,000 to ₹50,000 in the previous calendar quarter to unlock lounge access for the next quarter.

- Best Cards for Lounge: HDFC Regalia Gold and ICICI Sapphiro remain the most reliable for domestic and international terminals.

Zero Annual Fee Premium Credit Cards for Students

Students often think they aren’t eligible for the best premium credit card in India, but Secured Cards are the gateway.

- IDFC FIRST WOW: A lifetime free card issued against an FD of just ₹2,000-₹5,000.

- OneCard (Lite): High-tech app experience with no joining or annual fees. It helps students build a 750+ score before they even get their first job.

Which Bank Gives Credit Cards Easily to First-Time Users?

If you are a “New to Credit” (NTC) user, don’t apply for the most powerful credit card in India directly. Start where you have a salary account.

- HDFC & ICICI: They often give “Pre-approved” offers if you maintain a good balance.

- IDFC First Bank: Known for being “Beginner Friendly” with their lifetime free variants.

- Amazon Pay ICICI: If you are a heavy Amazon shopper, this is one of the easiest top 10 lifetime free credit cards in India to get approved for.

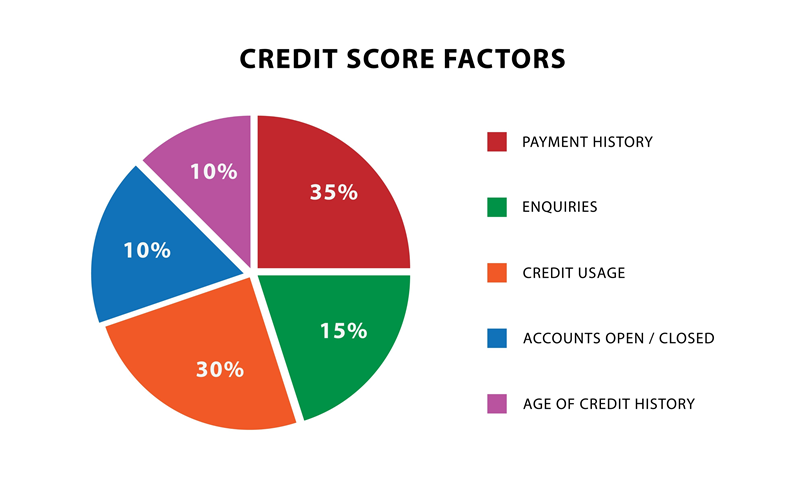

The 900 CIBIL Score Myth: What is the practical reality?

While the maximum CIBIL score is 900, reaching it is mathematically rare. It requires decades of perfect history, a flawless credit mix, and almost zero utilization.

What is the practical “High Score”? In the real world, less than 1% of people ever hit a score above 880. For most lenders in India:

- 750+ is considered “Excellent.”

- 800–830 is the “Practical Peak” for most disciplined users.

Once you cross 800, you already get the best interest rates and premium card invites. Moving from 820 to 900 doesn’t actually give you any extra financial benefits—it’s just a number for pride!

FAQs About Credit Cards & CIBIL

Does making a partial payment on a credit card bill drop your CIBIL score?

Technically, making a Partial Payment (more than Minimum Amount Due) does not directly drop your CIBIL score because it is still considered a timely payment. However, it leads to a high Credit Utilization Ratio (CUR) and heavy interest charges. If your utilization stays high for months, it indicates credit hunger, which can eventually lead to a decline in your score.

How can I get a lifetime free credit card without income proof?

If you don’t have salary slips or an ITR, the best way is to apply for a Secured Credit Card against a Fixed Deposit (FD). Banks like IDFC First, ICICI, and Kotak offer these cards instantly. Alternatively, if you have a strong relationship with your bank, they may offer you a Pre-approved card based on your average savings account balance.

What is the fastest way to increase my credit card limit?

The quickest way is to Request a Limit Enhancement through your banking app after showing 6 months of disciplined spending and full repayments. Another hack is to provide your latest hiked salary slip or ITR to the bank’s customer service, proving your increased repayment capacity.

Hidden Charges in Credit Cards: What do banks hide from us?

Banks often highlight rewards but stay quiet about:

Cash Withdrawal Fees: Interest starts the second you take cash from an ATM.

Forex Markup Fees: 2–3.5% extra on international or USD transactions.

Late Payment Interest: Not just a flat fee, but 36–42% annual interest on the entire balance.

GST: 18% tax on all fees and interest charges

What are the disadvantages of using a credit card for rent payments?

While it helps hit spend targets, it comes with costs:

Convenience Fees: Most platforms (and now banks) charge a 1%–2% fee + GST.

No Rewards: Many banks have stopped giving reward points on rent transactions.

Interest Risk: If you can’t pay the full bill, the rent (a large expense) will accumulate massive interest.

Which is the best zero forex markup credit card for international transactions?

In 2026, the IDFC FIRST Wealth or AU IXIGO credit cards are top choices for zero forex. For travelers, the Scapia Federal Card and Niyo Global are also popular as they charge 0% extra when you spend in foreign currency.

Does closing a credit card account damage your credit history?

Yes, it can. Closing an old card reduces your Average Age of Credit and your total Available Credit Limit. This makes your utilization look higher, which can cause a temporary dip in your CIBIL score. It is usually better to keep old, lifetime-free cards active.

How can I convert my credit card reward points into cash?

Most banks allow you to redeem points as Cashback directly into your statement through their NetBanking portal (e.g., HDFC MyCards or SBI Card app). Note that the value might be lower (e.g., 1 point = ₹0.25) compared to redeeming for flights or vouchers.

What are the pros and cons of a credit card against a Fixed Deposit (FD)?

Pros: Instant approval, no income proof needed, 100% approval rate, and helps build CIBIL from scratch.

Cons: Your FD is locked (you can’t withdraw it), and your credit limit is usually only 80–90% of the FD amount.

If a credit card fraud occurs, how can I get my money back?

Act within the Golden Window of 3 days. Report the unauthorized transaction to your bank immediately to block the card and file a Dispute Form. According to RBI guidelines, if you report within 3 days, your liability is zero. Also, file a complaint at cybercrime.gov.in.